October Wellness Spotlight

Financial Wellness

Talking about finances can be unpleasant. Money causes a lot of daily stress, and it can be so easy to avoid the topic of personal finance all together. If you are someone who avoids looking at your bank account, you are not alone. According to a Mind Over Money survey, 77% of participants reported feeling anxious about their finances. Avoiding the topic of finance is like avoiding opening your lunch container from Monday. The longer you avoid cleaning it, the worse it will get. In our October wellness spotlight, I am forcing us outside our comfort zone to face our finances head on in a discussion about financial wellness.

Defining Financial Wellness

There are many different definitions of financial wellness. The University of New Hampshire defines financial wellness as the ability to meet basic needs and manage money for the short- and long-term. Financial wellness is more than just having enough money in the bank. In fact, people of all levels of income report feeling the impact of financial stress. I guess the phrase “more money, more problems” might just reign true. More money won’t solve our problems if we still make the same financial mistakes. In today’s world, financial pressure is one of the leading causes of stress. Very few people are taught how to effectively manage their money, set financial goals, or build wealth. That’s where financial wellness comes in. It’s a lifelong journey that involves building the knowledge, habits, and mindset needed to make smart financial choices. Whether you’re just starting out, trying to get out of debt, or looking to grow your wealth, understanding the foundations of financial wellness can help you gain peace of mind.

Money Relationship

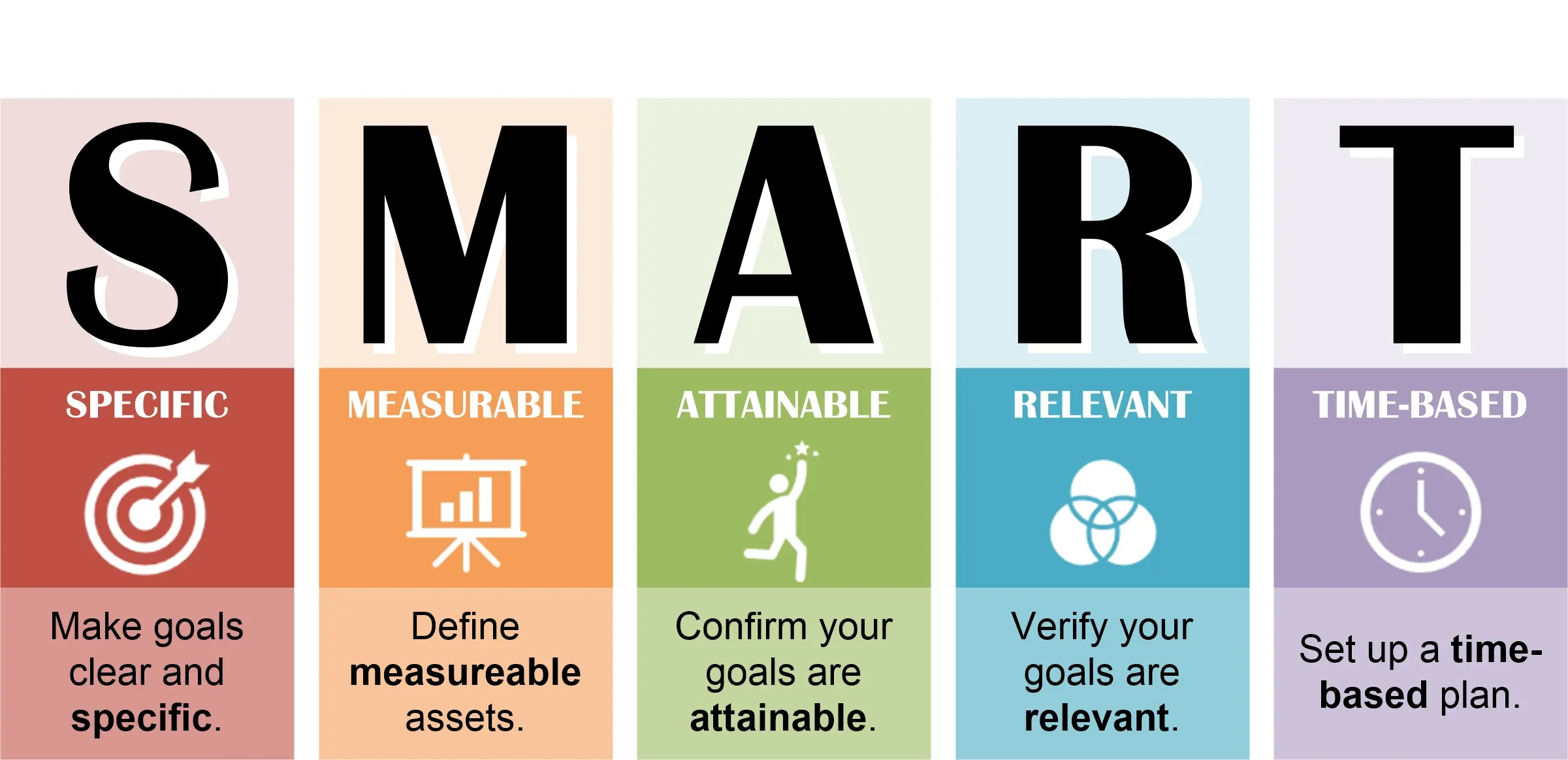

Let’s talk about our relationship with money. How we feel about money is often shaped by our upbringing, the culture that surrounds us, and our own past experiences. Some people grew up in households that were penny pinchers while others grew up in households that had no rules about finances. Both examples could cause someone to have an unhealthy relationship with money. Those who might qualify as the chronic savers might be a little more anxious about investing their money. On the other hand, someone who doesn’t grow up with any rules about finances might spend their money before it hits their wallets. Take a moment to think about how money was handled in your household growing up and compare that to how you handle money today. Understanding the psychology of money helps you identify these beliefs, shift unhelpful thinking, and make more empowered choices. Once we understand and can shift our mindset around money, we can start to set goals. SMART goals to be exact. Specific, Measurable, Achievable, Relevant, and Time-bound. By combining a healthy mindset with clear goals and consistent action, you set the foundation for lasting financial wellness. Here is a worksheet to start working on your financial SMART goals today.

Understanding your Cash Flow

Budgeting and managing your cash flow are essential skills for achieving financial wellness. At its core, budgeting is about understanding the relationship between your income (the money you earn) and your expenses (the money you spend). The goal is to ensure that your income consistently covers your needs, while also allowing room for savings, debt repayment, and enjoyment. Before we can start setting up a budget, it is important to understand where your money is going right now. Look through your bank accounts and make note of where money is going. You might find that you are spending a little too much money on take-out food or that you have subscriptions you didn’t remember you had.

Once we understand where our money is going, we can start to figure out a game plan. There are several types of budgeting methods that can help you take control of your money. A zero-based budget assigns every dollar a specific job. This means your income minus expenses equals zero, with no money left unaccounted for. Another saving technique is the 50/30/20. This divides your income into 50% for needs, 30% for wants, and 20% for savings or debt repayment. This rule might allow more flexibility. Finally, the envelope system is a hands-on, cash-based method where you divide money into physical or digital “envelopes” for each spending category to avoid overspending. For a more digital approach, there are different online bank accounts that allow you to automate your savings. For examples $50 a month can automatically be put into your savings account.

Emergency Fund

An emergency fund is one of the most important foundations of financial wellness. It’s a dedicated pool of money set aside to cover unexpected expenses like medical bills, car repairs, or cutting back on work hours. An emergency fund can be helpful to avoid relying on credit cards, loans, or falling into debt when life throws you a curveball. Having an emergency fund gives you peace of mind and a financial safety net, helping you stay on track with your long-term goals even during uncertain times. So, how much money should we save in our emergency fund? That number will depend on you and your family’s needs. A good starting point is typically $500 to $1,000, especially if you’re paying off debt. Once you’ve built that, aim for a full emergency fund that covers 3 to 6 months’ worth of living expenses, depending on your lifestyle, job stability, and family situation.

When it comes to storing your emergency fund, you want to make sure your money is in a secure location and is easily accessible when you need it. A popular method is using a high-yield savings account (HYSA). This is a type of savings account that allows your money to earn more interest than a regular savings account while remaining easily accessible when needed. HYSAs also uses compound interest which is your interest gaining interest. This can help your money grow on its own. It’s important that we avoid investing this money or keeping it in a checking account, as it’s meant to be stable, not risky or too tempting to spend. Building an emergency fund takes time, but $50 or even $25 a month into your emergency fund can make a big difference when life throws the unexpected at you.

Financial Game Plan

Creating a financial plan is about pulling everything together. This combines your budget, goals, insurance, and investments into one clear roadmap that guides your financial decisions. A strong financial plan gives you direction and purpose, helping you align your daily money choices with your long-term vision. It starts with a solid budget that tracks your income and expenses and supports your financial “SMART” goals like building an emergency fund, paying off debt, or saving for retirement. From there, you layer in important elements like insurance to protect against risk and investing to grow your wealth over time. As mentioned before, one powerful way to make your plan stick is by automating your finances. Whether that is for savings, paying bills, or even investing deposits. Setting up automatic contributions can help ensure consistency and remove the guesswork. It also reduces the risk of late payments or forgetting to save.

It’s important to remember that a financial plan isn’t a “set it and forget it” tool. Life changes and we may have to adjust our plan over time. Make it a habit to regularly check-in with your financial plan to review and revise your plan regularly, whether monthly, quarterly, or after major life events. By keeping your plan up to date, you stay in control, adjust to new challenges, and stay focused on building a secure and fulfilling financial future. These check-ins may look different for each person, and it is important to tailor them to your schedule and needs. It is also important to invite any necessary partners to your financial meetings. This could be your partner or spouse, a financial advisor, or maybe it is your children who are eager to learn about finances. It is important that we start getting comfortable facing our finances head on. Setting a good example for your children now can mean they grow up with a better understanding of financial wellness.

You’ve Got This!

You’ve Got This!

There are a lot of great local and national resources for you to tap into when it comes to financial wellness, and I have a few listed below. Work Well is currently putting on a Common Cents Challenge that focuses on how to implement the MyMoney 5 into their lifestyle to achieve a higher understanding of financial literacy. This is a free challenge for all faculty and staff to participate in. You can also check out UND Office of Human Resources page for information on payroll and taxes.

Taking care of your financial wellness is a big step in the direction of taking care of yourself and your loved ones. I understand that finances are scary to think about today, but I want you to know that you can do hard things. Facing our finances head on can allow you to gain peace of mind, reduce stress, and build a brighter, more secure future. Remember, financial wellness isn’t about being perfect; it’s about being consistent and intentional. Every small step you take, whether it’s setting a budget, saving $10, or paying off a small debt, you should be proud of the progress you have made. You don’t have to do it all at once. Just start where you are, use the tools available to you, and keep going. Your future self will thank you.

Resources

Work Well – Common Cents Challenge

Nerd Wallet – High Yield Savings Accounts

References

University of New Hampshire – Definition Financial Wellness

Nerd Wallet – Zero-based budgeting